A recent Princeton University analysis shows that top U.S. schools continue holding fossil fuel assets despite the divestment movement’s claims that they have been victorious in getting these institutions to divest.

The analysis, presented on Monday, March 21st at the Council of the Princeton University Community (CPUC) meeting, is part of the school’s efforts to adopt a climate-oriented investment policy in its endowment. It examines the investment status and recent policies of the top 20 U.S. School Endowments. However, the analysis contradicts the supposed “wins” that the divestment movement has championed over the last couple years. In fact, these schools have rarely adopted full divestment.

Harvard, Stanford and Princeton still hold fossil fuel-related assets

Three out of the top four universities with the largest endowment funds – a collective $127.4 billion in 2021 –continue holding fossil-fuel related assets, mostly via indirect funds:

For instance, of the $37.7 billion in Princeton’s endowment alone, $13 million is directly invested in fossil fuels. The remainder of Princeton’s fossil fuel assets are tied up with indirect exposure, some of which run through multi-sector funds.

In fact, the analysis suggests that holding assets via indirect investments is a model commonly implemented by the top 15 U.S. universities included in the analysis.

Indirect investments reflect the dynamics of the financial sector

The argument for divestment efficacy is further diluted as the analysis shows that endowments “overwhelmingly skew” towards indirect fossil fuel investments through sector-focused funds or broadly mandated investment funds. Fossil fuel exposure through broad “commingled funds” highlight the vital nature that they play today and in the foreseeable future, housing equally paramount sectors and companies under the same umbrellas.

In fact, only two out of the 20 universities in the analysis have pledged commitment to full divestment, both of which are accompanied with target dates to allow for re-balancing of indirect holdings that include fossil fuel assets.

The energy future is a transition, not divestment and disassociation.

As the world still heavily relies on traditional energy sources, it would be irresponsible to scalp fossil fuel-related assets for politically driven reasons. Instead, the responsible measure would be to work with institutions and energy companies alike to increase investment in the climate technologies of the future and establish appropriate phasing periods as capabilities change.

During the Princeton CPUC meeting, President Eisgruber expressed the competency that must be understood in order to ensure a successful energy transition that maintains reliability throughout:

“I think what I would do just once again, is to remind folks that the process that we have at the University of harboring questions around dissociation and divestment, that it’s a process that focuses on the long-term values of the University and decisions reached designed to be long term kinds of judgments.”

At a time when so many, regardless of political affiliation, are calling for increased oil and gas production to bring down high energy costs, stripping the oil and gas industry support by way of pressuring or banning investments would not only harm the well-being of the companies that produce energy, but the general public that counts on these sources in more ways than they even realize. This practice alone would be irresponsible, but conforming to divestment demands at the hand of unjust and unrealistic rationales would be reckless.

Amid vocal calls for divestment, experts and financial leaders continue to affirm that engagement drives change. Endowment decision-makers and asset managers are following this plan for climate action, as their vested interests remain with the energy sector. To continue the cause of finding climate solutions, two cases in point – Harvard President Lawrence Bacow’s non-divestment climate announcement and BlackRock Chief Executive Larry Fink’s annual letter to CEOs – provide guidance how to navigate around activists’ demands

Harvard, from engagement model to communications misprint

Throughout the year, divestment announcements were more optics than actions, aimed at perceptions for prominent institutions. Too often, institutions used these opportunities to announce shifting investment strategies – thus, giving the guise of divestment against the reality of no action.

In Harvard’s case, Harvard President Bacow issued a status quo letter to the university community which included no new information regarding strategic environmental or divestment goals. It was already known that Harvard Management Company (HMC) outlined a path to decarbonize the endowment and commit a net-zero greenhouse gas status by 2050. So begs the question – why were climate activists to so quick to claim victory when President Bacow’s letter states that Harvard’s actions do not constitute divestment?

Despite headlines claiming this move as divestment, the only real action Harvard took was to dissolve some limited partnerships, with no disclosed timeline of doing so. The possibility for Harvard to retain assets in the fossil fuel industry for the next 20 to 50 years, or even longer, still remains. This mischaracterization of Harvard’s actions versus reality is significant for the overarching divestment landscape – the understanding of nuance matters if other schools or funds are considering the measure, or even following suit behind Harvard.

Top U.S. Colleges are Still Investing in Oil and Gas

While some colleges made similar moves, the majority of colleges have turned down divestment calls, maintaining investments in the oil and gas sector. Aside from Harvard University, five out of the top eight institutions with the largest endowments have not committed to divestiture of any kind and collectively allocate roughly $101.4 billion in financial assets.

Rather than divest, many Ivy League and other institutions have led efforts on helping to develop climate solutions through industry partnerships, programs and global climate goals. In particular, Princeton University has stepped up by using fossil fuel funding to commission research for reports that outline net-zero framework and by utilizing their experts to contribute to the global discussion – most recently at the United Nations’ COP26 summit – on adequate actions going forward, none of which include pure divestment.

COP26 experts agree that the industry is part of the solution

COP26 led the development of a new goal for creating a process around transparency and quantified climate financing goals by 2024. In fact, financial experts agreed that collaboration with the industry is paramount if we want to speed up climate solutions.

During the week of COP26 a climate finance-focused panel was held by the Green Finance Institute and City of London that featured Larry Fink of BlackRock and Lord Mayor of London William Russell. The conversation between these leading voices in the financial space focused on the importance engagement over divestment to affect meaningful change.

Fink, CEO of one of the world’s largest asset managers, expressed that pulling out of fossil fuel investments would be a mistake and that, in fact, hydrocarbon companies will be vital to reaching the climate solution. The BlackRock CEO iterated the importance of a fair and just energy evolution where continued support of the oil and gas industry should lead us further down the path to cleaner fuel production and solutions. His perspective came through loud and clear:

“Let us be clear, hydrocarbon companies are part of the solution, they are not the problem and the one key message I am here for is, if we are not working with the hydrocarbon companies, we will never get to net zero.” – Larry Fink, Chairman and CEO, BlackRock

Given the amount of thoughtful participation by financial institution executives, the global finance industry is more engaged than ever in actively searching and collaborating for solutions.

The year of financing and framework lies ahead

In 2022, we can expect a pivot towards the comprehensive build-out of framework for sustainability finance processes, investor behavior research and scrutiny around transparency and disclosure rules regarding climate-impacting company operations. To do so, financial experts are bringing forth relaunched expectations in favor of collaborating with the industry:

“Divesting from entire sectors – or simply passing carbon-intensive assets from public markets to private markets – will not get the world to net zero. And BlackRock does not pursue divestment from oil and gas companies as a policy.” – Larry Fink, Chairman and CEO, BlackRock

As we advance ESG investing and collaborate toward real climate and energy solutions, perhaps we can finally bid adieu to divestment – and ineffective tactic that achieved nothing in 2021.

Harvard University President Lawrence Bacow has been praised by divestment supporters after releasing a public letter connecting climate change to Harvard’s investment strategy. The trouble is that neither Bacow’s letter, nor his team, ever mentioned divestment.

Bacow’s letter shows the need to focus more on solutions than empty gestures, where industry and academia are partners in the energy transition. A push for divestment at this stage would only impede this effort—while also costing students and schools money.

Partnership, Not Divestment

Harvard’s decision allows for future engagement with the energy industry, following a path taken by Princeton earlier this year. While university communications de-emphasize the role of fossil fuels—and indeed natural resources more broadly—in its investment holdings, the HMC is pursuing a goal of achieving net-zero emissions by 2050.

In it’s Climate Report, HMC wrote:

“Harvard’s commitment to transition its endowment to net-zero GHG emissions by 2050 transcends the binary divestment debate by focusing on portfolio management—on both the supply and demand side of a fossil fuel-reliant economy—with a clear, intentional effect. This commitment complements Harvard’s extensive work in research and scholarship to address climate risk and represents a critical shift towards a holistic campaign to tackle the root causes of accelerating climate change.”

Universities that have announced stringent divestment procedures often find these policies difficult to implement because of the complex nature of some of the funds they hold and the value of partnering with the industry in finding actual solutions within the energy transition.

This is something Princeton recognized earlier this year, when it released new investment criteria that “disassociated” from some companies but stopped short of supporting divestment.

In May, the Princeton CPUC Resource Committee released a set of recommended principles to guide the Committee on Finance of the Board of Trustees in investment decisions. These recommendations included disassociating from the highest greenhouse-gas-emitting sectors of the economy, but acknowledged the need to continue to work with industry:

In its principles, the Resource Committee wrote:

“The fossil fuel industry has been the primary supplier of energy upon which the global economy is currently based. Immediately cutting off the supply of fossil fuels is both unrealistic and potentially harmful to global communities. This concept also applies to Princeton dissociating from the fossil fuel industry: It is not possible to completely dissociate from fossil fuels in the short term.”

For instance, as part of its ongoing work with industry to address the energy transition and climate change, Princeton’s Andlinger Center for Energy and the Environment is partnering with ExxonMobil on research into next-generation energy and environmental technologies.

MIT Energy Initiative is working on developing low-carbon solutions along with Shell, ExxonMobil and Eni. Stanford’s Strategic Energy Alliance is a industry-academia research program to accelerate the transition to affordable, low-carbon energy systems. Founding members include Shell, ExxonMobil and Total.

Research work like this will be crucial to addressing the impacts of climate change in the years to come, and today’s partnerships will pay large dividends in the future.

Little Impact To Harvard’s Endowment

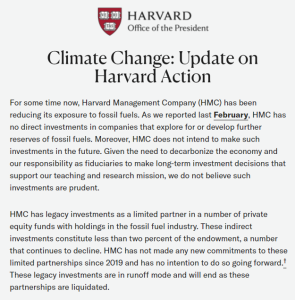

While some categorized comments out of Harvard as a turning point, the reality is Harvard has done little to change its position nor its investments. As Divestment Facts has pointed out before, Harvard Management Company disclosed in February that less than 2 percent of the school’s endowment was invested in fossil fuels.

In its first-ever Climate Report HMC wrote:

“HMC has reduced its overall exposure to fossil fuels — including both direct commodity investments as well as indirect investments in companies that explore for or develop further reserves of fossil fuels held through dedicated externally managed funds — from approximately 11% of the portfolio at the end of fiscal year 2008 to less than 2% at the end of fiscal year 2020, a decrease of more than 80%.”

In the recent letter, Bacow acknowledged that HMC had “legacy investments” comprising a small percentage of the overall endowment “with holdings in the fossil fuel industry.” These investments are the sticking point for pro-divestment activists.

But what are they?

What is a legacy limited partnership?

Legacy investments are assets that the HMC holds through limited partnership private equity funds, generally for a fixed term of 10 years. With the timeframe of these types of investments considered, it should be known that Harvard will remain in its private equity funds for an undisclosed number of years, until they are set to expire. Withdrawing the funds before the investment matures would cost the endowment money.

Still, waiting for private equity funds to mature over the next decade is hardly a full-throated endorsement of divestment. In fact, it’s quite the opposite, since Harvard is not actively trying to liquidate these assets.

Harvard Magazine John Rosenberg had this point in a recent op-ed questioning Bacow’s letter. Referring to the HMC’s Climate Report, Rosenberg argued that investment returns, not pro-divestment sentiment, motivated the HMC’s actions.

Rosenberg wrote:

“…those changes were part of a concerted effort to overhaul the portfolio and HMC’s operations. In an attempt to improve investment returns, HMC has disposed of and otherwise deemphasized commitments to various commodities and real assets (presumably, fossil fuels, but also extensive holdings in timber and agricultural land), and to such asset classes as real estate. All of this was widely publicized as part of HMC’s stem-to-stern overhaul, driven by investment performance.”

Given its limited impact, its surprising the investment decision has attracted as much attention as it has.

The value of dialogue

Divestment proponents have been against working to find a middle ground with school authorities, despite faculty members as well as financial experts objecting to divestment’s quick-fix approach to the climate crisis.

Most recently, Yale University Sustainable Finance Professor Cory Kroninsky, called divestment a “waste of time” that did not have a meaningful impact on climate. The lack of a balanced conversation has curtailed the movement’s potential to actually made progress on climate research or even join forces with the industry to find better climate solutions.

Not only that, but divestment has also failed to discuss its direct impact to consumers and communities that rely on affordable energy and well-paid jobs. As one Harvard student wrote this week, “the livelihoods of many other people are also currently tied to fossil fuels.” A path forward is more complicated than divestment offers.

Bottom line

Divestment will always make headlines, but the focus on real solutions is where academia can play the greatest role in supporting actual benefits for the environment. The Harvard and Princeton examples show that school administrators recognize the value of working relationships with industry. Today’s energy companies are deeply invested in supporting the energy transition. Severing all ties with the conventional energy industry would only limit these schools’ capacity to support this goal.

Going ‘Beyond Divestment’ means that Harvard recognizes the emptiness of the divestment narrative, and its ability to drive any real change.

The energy transition will be an extended process, one that requires the expertise and experience of a wide variety of industries. The companies that already work to power homes, cars, planes, and industry are a critical part of a path forward. However, today’s divestment discussion all too often leaves them out of the conversation.

Let’s take for example tech mogul and philanthropist Bill Gates, who after previous opposition to divestment recently sold direct holdings in oil and gas companies in 2019. Gates has long acknowledged it’s hard to dismiss an industry “worth roughly $5 trillion a year and the basis for the modern economy” from the energy transition. Unsurprisingly, Gates’ provided important context for his decision, highlighting that sustainability includes energy companies:

“Getting to zero [emissions] doesn’t mean we are going to stop doing the things we are doing—flying, driving, making cement and steel, or raising livestock.”

The view put forward by Gates and many others highlights the array of alternatives beyond divestment that can provide tangible investments in sustainability and ESG.

Engagement over divestment

As financiers continue to invest in ESG, many have also acknowledged the role oil and gas companies will play in the low-carbon transition. Bloomberg financial writer Nathaniel Bullard lays out his view on the value in continuing to invest in these companies:

“Now it’s clear the focus should be less on divestment from the fossil fuel sector and more on reallocation to companies that are planning to create value from the low-carbon transition. That doesn’t necessarily exclude the energy sector.”

Others, like BlackRock, are firm believers that engagement should be the first response:

“Much of BlackRock’s $8.7 trillion in assets are in passive funds that track indices. That’s one reason why BlackRock steers clear of using the threat of divestment for companies whose climate policies are lagging. Instead, it focuses on engaging with the company first and uses shareholder votes as a last resort.”

In addition, respected voices within the financial services sector have called out divestment a short-sighted strategy. Financiers’ steady opposition to divestment is mostly due to the tactic’s inefficiency in bolstering change while dismissing the possibility of high direct and associated costs with divestment.

Moody’s, the world’s top credit rating agency, argued that divestment was “not a significant factor” for fossil fuel companies’ finances. Commenting on the movement in a white paper, the CATO Institute echoed similar remarks about divestment being pointless, arguing the value of stocks and bonds have already incorporated potential risks, hence, divestment has no power at all.

Focusing on Actions over Empty Gestures

Updating asset evaluation metrics based on ESG criteria has also picked up quickly among endowment and pension funds. Back in December 2020, New York State Comptroller Thomas DiNapoli announced a net-zero emissions plan across its investments by 2040. While the net-zero model has been adopted widely across industries, including Harvard University, the novelty of DiNapoli’s approach was around the asset review process.

Instead of embracing divestment, DiNapoli committed to review and establish a baseline criterion by which to judge investments in certain sectors. Simply put, companies will be assessed depending on their efforts and progress, not a blanket political choice.

Ultimately, and unlike divestment proponents that refuse to find a middle ground, DiNapoli has always welcomed engagement and collaboration:

“The risks of climate change, greenhouse gas emissions, controlling them and reducing them is not a question of selling stocks on fossil fuel companies. Every, every entity, organization, corporate sector, we all must be part of that conversation.”

Industry Fueling Opportunity

In the past decade, traditional oil and gas companies were ahead of the curve, planning for a low-carbon world and investing in research for alternative energy technologies. Often, these partnerships include industry-funded research projects focused on environmental and alternative energy research.

Faculty members at Stanford have defended research partnerships built with the oil and gas industry. In Geophysics Professor Dustin Schroeder’s words: “funding from fossil fuels supports a lot of environmental and alternative energy research on campus”.

Likewise, Lynn Loo, Director of Princeton’s Andlinger Center for Energy and the Environment, has defended the university’s partnership with fossil fuel companies. Loo urges the need to reach net-zero emissions as quickly as possible, and that this cannot be done without partnering with the oil and gas sector. In the case of carbon sequestration, Loo argues, “Exploring the most viable methods for “carbon capture and storage” necessarily involves oil and gas companies.”

Loo also highlighted how the Center’s partnerships with fossil fuels have allowed them to develop crucial research in energy efficiency, electrification, renewables, hydrogen and bioenergy.

Bottom line: It’s time to focus on investments, not divestment. Loren Cohen, Professor of Business Administration at Harvard Business School, points out that fossil fuel companies “are investing about three times more than the average firm in climate change mitigation technology.”

Is that really something to divestment from?

Over the last year we saw a flurry of divestment activity that is indicating where the movement is headed. From coast to coast, many colleges remained opposed to taking on activists’ calls for divestment. Some, however, did not.

Here’s a review of the major divestment themes we saw in the crazy year that was 2020, and what we can expect in the year ahead.

High Profile Announcements Without Much Bite

One of the biggest surprises of the year was in-fact not from the Ivy Leagues, but from Georgetown University, located in the heart of the nation’s capital.

Back in February, Georgetown announced that by 2030 it would not be making any new investments in fossil fuels. It also stated it would remove any current fossil fuel holdings from its investment portfolio as well. Initially activists cheered in support of the administration’s announcement. But, in hindsight, this can’t help but seem like just another empty gesture.

A few months later, the student newspaper reported that despite this high profile pledge, Georgetown remained heavily invested in the fossil fuel industry, and would be so for some time due to the complicated nature of purging portfolios of an entire economic sector.

Speaking of empty gestures, Georgetown was not the only academic institution to make a quasi-divestment announcement in 2020 either. George Washington University announced it would divest within the next 5 years. Cambridge University, Brown, and Oxford also heeded to years of pressure by activists and announced they would divest as well. That’s about it in terms big-name institutions who made full-out commitments to eventually divest from fossil fuels.

Some Big Time Rejections

And while a handful of schools said they would divest; many came out in opposition, some for the third or fourth time. Harvard, Yale, Princeton, Stanford, Boston College, are a handful of institutions, just to name a few. However, in 2020 specifically, more and more institutions opted against full divestment and instead chose a more realistic policy of investing in sustainability. Thus, for 2020, institutions and pension managers laid out the foundation for the net-zero emissions movement. Essentially, it’s a commitment to do exactly as it implies; by a certain date all investments and energy consuming activities will have net-zero carbon emissions, without excluding nor rejecting fossil fuels’ involvement.

The Harvard Approach. An environmentally sound policy that doesn’t play politics

Harvard has consistently rejected divestment for years. So, what made this year any different from the rest? Back in April, Harvard was one of the first institutions to develop an alternative net-zero approach to investing versus blanket divesting. In a letter penned by The Harvard Corporation and President Bacow, Harvard essentially tasked the group responsible for overseeing Harvard’s endowment to devise a plan that would achieve net-zero greenhouse gas emissions by 2050 and present that plan to the Harvard Corporation by the end of 2020.

And although a full disclosed plan is not publicly available yet, Harvard continues favoring engagement and collaboration over divestment. For instance, Harvard’s own endowment managers have hinted that further research and partnership with the industry is needed to advance carbon sequestration technologies to offset emissions.

Financial experts have been clear on divestment’s inefficiency. Collaboration is a sounder strategy.

Unlike some who urge full and immediate divestment despite the costs, financial experts, luckily, acted as the voice of reason in 2020. Divestment, a financial decision, requires a deep understanding of markets dynamics and asset management to provide sound economic advice.

To start with, Moody’s, the world’s top credit rating agency, reported that divestment was “not a significant factor” for fossil fuel companies’ finances, discrediting climate activists’ claims about the miraculous financial effects of divestment over oil and gas companies.

What’s more, financial experts have not only called divestment pointless. From a very practical, business perspective, they’ve acknowledged the role the oil and gas industry will play in achieving the low-carbon transition. For instance, Bloomberg | Quint’s financial writer Nathaniel Bullard sees value in continuing to invest in these companies:

“Now it’s clear the focus should be less on divestment from the fossil fuel sector and more on reallocation to companies that are planning to create value from the low-carbon transition. That doesn’t necessarily exclude the energy sector.”

In a similar fashion, during the World Pension Summit 2020, asset owners and financial experts agreed that it was more important to engage with the industry than to divest. In fact, focusing exclusively on punitive measures like divestment “was not the desired course of action to ensure responsible investing”.

Either from a pure business strategy, or because you are truly interested in funding the next low-carbon technologies, divestment isn’t the right way to go.

Divestment’s crowning achievement is simply not divestment

New York’s pension funds have a bone to pick with proponents of divestment. For years, both New York state and local pension funds have been an area of focus by anti-fossil fuel activists pushing for divestment.

So when New York State comptroller, Thomas DiNapoli, introduced a 2040 net-zero emissions plan in December, divestment advocates quickly called this an absolute win. However, they forgot to read the fine print. In fact, DiNapoli’s plan is a review process to establish baseline criteria to judge investments in certain sectors. Not a commitment nor an announcement to divest.

DiNapoli has fiercely defended his fiduciary duty and avoided the divestment path at all costs. In his view, the plan announced is a commitment to make the NYS pension fund’s investment policy more sustainable without compromising the assets of over 1.1 million New Yorkers. Divestment instead would be the irresponsible approach.

Conclusion:

Full divestment is a thing of the past. Top universities, state and local pension funds and financial experts agree that divestment is both ineffective and insufficient to address climate change concerns adequately. However, moving forward we expect more flexible decisions like that of Harvard and the New York State pension fund, capable of integrating higher sustainability standards while continuing important research and technology opportunities with the industry.

Harvard President Lawrence Bacow announced on April 21 that the Harvard Corporation has directed the Harvard Management Company “to develop a plan to achieve net-zero greenhouse gas emissions by 2050” and to prepare to present a plan to the Corporation by the end of 2020. Here are the five things you need to know about the announcement.

1) This is not divestment. Period. President Bacow states the following:

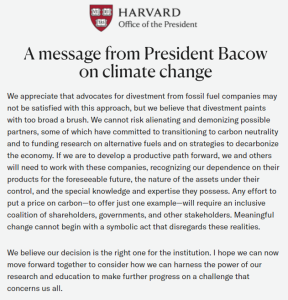

“We appreciate that advocates for divestment from fossil fuel companies may not be satisfied with this approach, but we believe that divestment paints with too broad a brush. We cannot risk alienating and demonizing possible partners, some of which have committed to transitioning to carbon neutrality and to funding research on alternative fuels and on strategies to decarbonize the economy. If we are to develop a productive path forward, we and others will need to work with these companies, recognizing our dependence on their products for the foreseeable future, the nature of the assets under their control, and the special knowledge and expertise they possess. Any effort to put a price on carbon—to offer just one example—will require an inclusive coalition of shareholders, governments, and other stakeholders. Meaningful change cannot begin with a symbolic act that disregards these realities.”

2) Divest Harvard is once again only looking for politicized divestment, not solutions. According to the group, the “announcement falls far short of divestment” and “by not including divestment as one of its commitments today, Harvard is continuing to provide social and economic capital to the forces standing in the way of a decarbonized future.” The group goes so far to say “By evading divestment, Harvard is once again standing with fossil fuel companies and against its students’ futures,” pledging to double down on divestment efforts in days ahead. This announcement only crystallizes the goals of the divestment movement: make symbolic, political statements regardless of tangible environmental solutions.

3) Harvard is looking at actions, not empty gestures. Harvard is avoiding divestment. Why? Because it is an act that does nothing to support the environment, a fact that President Bacow, former President Drew Faust, and numerous Harvard faculty and students have stated previously.

Just today, Professor of Environmental Policy at Harvard John P. Holdren stated his opposition to divestment, noting “It’s counterproductive because it would lead many Harvard faculty and students to imagine they’d struck an effective blow against climate change—and would likely reduce their focus on more productive measures—when it would actually be a misdirected blow. Just advocating for it is distracting people from measures that would actually be effective.”

4) This announcement is not a surprise. The call for this kind of reporting aligns with the University’s now-official support of the Task Force on Climate-Related Financial Disclosures, the Paris Agreement, and broader on-campus sustainability efforts. Does it mean giving up investments in energy companies? No. It means beginning a process to assess investments and consider options.

Every industry uses energy and, in turn, this review will look at the entire carbon footprint of the portfolio from an array of sectors. As Professor Holdren stated, “If university divestment of fossil-fuel companies were a good idea, surely divesting from all companies that use fossil fuels would be a much better one. Of course, that would entail divestment of virtually all companies in the portfolio.” President Lawrence Bacow has also agreed that working with the industry and fostering research is the best tactic, noting “engaging with industry to confront the challenge of climate change is ultimately a sounder and more effective approach for our university.”

5) The endowment is for students, who will need it more than ever. As this process unfolds, the role and value of the endowment cannot be put aside. An endowment is there to support students and programs, not make political statements. Harvard’s leaders have long stood by this fact. As this process unfolds, the role and value of the endowment will be paramount. Former President Drew G. Faust expressed concern about using the university’s endowment as a political weapon for exactly this reason, stating “I don’t think the endowment should be used for exerting political pressure. It is meant to fund the wide range of activities that the University undertakes. As we said before, 35 percent of our operating budget comes from the endowment. It should not be used as a weapon to exert pressure on one group or another.”

A new editorial in the Boston College student newspaper, The Heights, calls on the college to divest, running in contradiction to the many on-campus and nearby voices that say no to this costly, ineffective effort.

For starters, leadership at Boston College has made it clear they have no plans on moving divestment forward. “Boston College remains opposed to divestment from fossil fuel companies on the grounds that it is not a viable solution to the important issue of climate change,” states Public Affairs and university spokesperson Jack Dunn in February 2019. The remarks reiterate the schools 2015 position, that “[Divestment] would be done if there is a clear compelling case that shows a particular company is doing something unethical. We do not think that companies that are engaged in energy production are engaged in unethical conduct.”

Fellow nearby student newspaper the Harvard Crimson also spoke out against divestment in 2017:

“We have expressed our criticism for the strategy of divestment many times in the past. Though the specific demands of Divest Harvard have changed, their underlying philosophy toward combating climate change has not. Simply put, it is the supply of and demand for fossil fuels that creates the market valuations of energy companies, not the reverse. Divestment has no ability to alter these basic economic realities.”

The paper’s comments echo sentiments from former and current leadership at Harvard. Harvard student, Wesley Donhauser, just this month notes divestment is purely a distraction from real solutions in the New York Times:

“While I share Ms. Lockwood’s concerns about climate change, divestment is little more than financial theater. Even at its best, it would have no meaningful effect on global emissions. What is worse, divestment misconstrues the climate problem and distracts from the market-based solutions that can actually make a difference.”

University President Lawrence Bacow also continues to object to divestment, stating:“

“The endowment exists to support the institution, to support our students, and to support our faculty. And it was on those terms that our donors have entrusted the resources to us. They’ve said here, here are these resources which we want you to invest to support these activities—not to accomplish some other ends.”

Leaders at neighboring MIT have also called out divestment as an act that would “entangle MIT in a movement whose core tactic is large-scale public shaming,” with Northeastern rejecting divestment on the grounds it is “an institution that actively engages with the world, not one that retreats from global challenges.”

Massachusetts is no stranger to the divestment topic, but it is clear its universities are saying no to this all cost, no gain gesture.

In the New York Times this week, a Harvard student, Wesley Donhauser, lays out exactly why divestment is a false solution for universities and endowments. In his words, divestment is a purely a distraction from real solutions:

“While I share Ms. Lockwood’s concerns about climate change, divestment is little more than financial theater. Even at its best, it would have no meaningful effect on global emissions. What is worse, divestment misconstrues the climate problem and distracts from the market-based solutions that can actually make a difference.

This Harvard student instead advocates for solutions and policy changes over costly empty gestures, continuing “Instead of demonizing fossil fuel companies, we need economy-wide incentives that encourage all parties to do the right thing.”

His last line: “Substitute symbolic posturing for a real solution? That would move Harvard — and the world — forward.”

We couldn’t have said it any better. This is the type of action all universities should focus on.

As the divestment movement grinds to a halt in the wake of continued rejections, those with concerns about the environment should be glad to see pressured entities focused on real solutions over empty gestures. While universities have been quick to dismiss divestment as ineffective and fiscally irresponsible, they have undertaken significant programs to green their campuses and cut their carbon emissions—initiatives which, unlike divestment, will actually have a positive impact on the environment. Perhaps unsurprisingly, Harvard University is leading the charge.

Why Harvard Won’t Divest

Like the vast majority of universities, Harvard has resisted activist pressure and rejected divestment over and over again. In fact, Harvard’s former and current presidents have been outspoken in their opposition to the policy, albeit for different reasons. Former President Drew G. Faust was primarily concerned about using the university’s endowment as a political weapon, stating:

“I don’t think that divestment is an appropriate tool, because I don’t think the endowment should be used for exerting political pressure. It is meant to fund the wide range of activities that the University undertakes. As we said before, 35 percent of our operating budget comes from the endowment. It should not be used as a weapon to exert pressure on one group or another.”

More recently, University President Lawrence S. Bacow highlighted another issue: the fact that divestment won’t actually reduce anyone’s carbon footprint and a university with Harvard’s resources and talent can do better. As the Harvard Crimson described, Bacow believes “not only is divesting to compel change improper, he said, but it is also impractical and ineffective.” In his words:

“I think there are far more effective ways for us to influence social policy, and public policy, as well, through our research, our scholarship, through our teaching. And I think in the case of fossil fuels, we’re doing exactly that.”

Furthermore, he notes that the best path forward will likely involve working with the world’s energy companies, not against them.

“It’s also the case that if we want to bring about meaningful change—as I think we should—in trying to help create clean paths to energy, that we need to be willing to work with those organizations and institutions that are responsible for the infrastructure that literally fuels our economy.”

President Bacow also highlights as many other universities that divestment stands in direct opposition to the universities approach to finding solutions:

“It strikes me as hypocritical to say we’re willing to work with you, we’re willing to do research with you, we’re willing to engage with you, we’re willing to buy your product, while at the same time saying but we will not consider owning your stock.”

While such cooperation may put-off divestment activists, its far more likely to deliver real, tangible solutions that are realized when universities and world-class energy companies are able to work together.

Thankfully, this kind of cooperation is already occurring in university labs across the country, for example, Exxon Mobil is partnering with MIT to research carbon capture, utilization, and storage (CCUS) technologies, with Princeton to explore solar and battery technologies, and with University of Wisconsin-Madison to research converting biomass into transportation fuels. As for Harvard, it is partnering with Exxon Mobil on methane research. But that’s not all the university is doing.

The Ivy is Getting Greener

Harvard has made ambitious pledges to cut its carbon emissions and improve the overall sustainability of its campus and supply chains. According to the university’s designated sustainability website, Harvard intends to bring its students, faculty, and staff together,

“to use the campus and… surrounding community as a test bed to incubate exciting new ideas and pilot promising new solutions to real-world challenges threatening the health of people and the planet—at Harvard and across the world.”

And how does this lofty goal manifest itself? Not by divesting, but in fact, investing into clean energy research. Here are a few examples:

In addition to these investments, the university has spearheaded green living and green office programs on campus to educate students and residents living and working on campus on sustainable practices and behaviors, undertaken a project to aggressively cut lab emissions, and installed on-site solar PV, solar thermal, biomass, wind, and geothermal installations.

It’s a safe bet that these efforts, as well as the efforts of like-minded universities, will yield far greater progress in reducing greenhouse gas emissions than fossil fuel divestment, a wholly-symbolic gesture.

The Heartland Institute and Bloomberg recently reported that the managers of Harvard’s endowment lost a whopping $1 billion by prioritizing “feel good” investments over ones that consistently generate solid returns. These losses, along with the stunning $8.5 billion losses that CalPERS faced after pursuing a divestment strategy, fly in the face of activist claims that ideology-based investing is as profitable as traditional investment strategies.

While the losses are significant there is a greater issue at stake here: the question of whether fund managers are violating their fiduciary duty by making politically-motivated investment decisions, instead of focusing solely on maximizing returns. Many experts believe they have. For example, the U.S. Department of Labor, which oversees retirement plan funds, released new guidelines at the end of April that stated:

“…because every investment necessarily causes a plan to forego other investment opportunities, plan fiduciaries are not permitted to sacrifice investment return or take on additional investment risk as a means of using plan investments to promote collateral social policy goals.”

And as energy expert Paul Driessen of the Heartland Institute put it:

“It seems to me the money managers followed their own agendas while violating their fiduciary responsibilities to the university they were supposed to serve…The bottom line is Harvard had a fiduciary responsibility to invest wisely and earn money for the school instead of losing a billion dollars in pursuit of politically fashionable, green pursuits.”

Even though Harvard is not remotely short on cash, it’s endowment’s recent performance has been deeply troubling compared to its peers. In fact, according to Bloomberg, its 10-year average annual return is just 4.4% compared to 6.6% at Yale, 7.1% at Princeton, 7.3% at Columbia and 7.6% at MIT.

Harvard’s administrators recognized pretty quickly that fossil fuel divestment was a terrible policy, and chose to protect students and faculty from the inevitable cost of divesting the endowment. In the words of former Harvard President Drew Faust:

“I don’t think that divestment is an appropriate tool, because I don’t think the endowment should be used for exerting political pressure. It is meant to fund the wide range of activities that the University undertakes. As we said before, 35 percent of our operating budget comes from the endowment. That is why people gave their funds to create the endowment. It should not be used as a weapon to exert pressure on one group or another.”

Let’s hope this Harvard recommits to emphasizing returns, not spurious political gestures, with their endowment and remembers that appeasing emotional pleas may, ultimately, cost them big bucks.

All quotes featured by professors and school leaders on this website are public statements made by individuals and are not necessarily representative of the institution of which they are associated. Said schools and universities are also not affiliated with IPAA or DivestmentFacts.com.